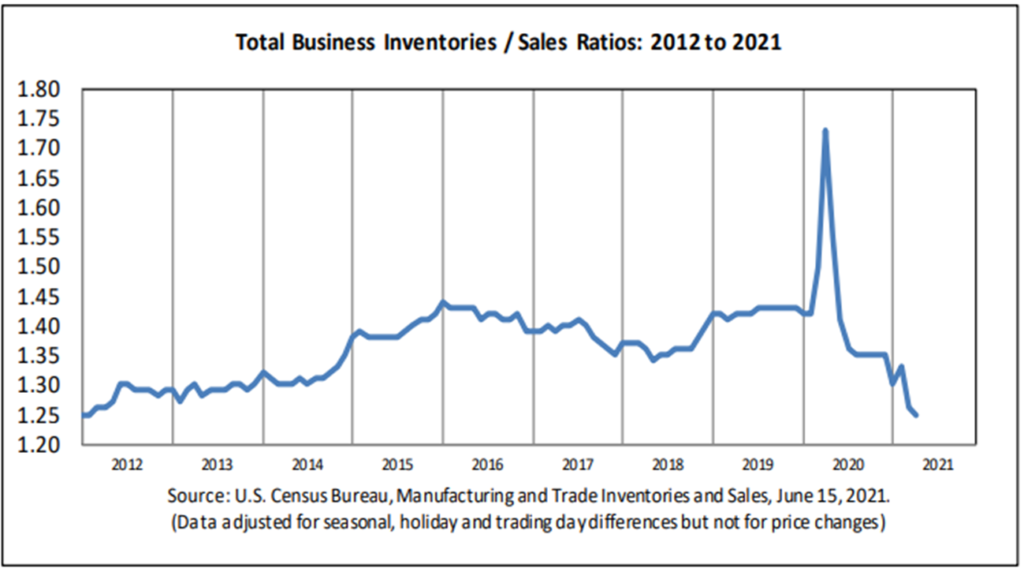

This is not news. But the duration and depth of the disequilibrium is cause for concern. Above is what the US Census reports for April and prior. The May report will be released next week. Any bets on turning up or continuing down?

Despite Census bureau statistics, grocery distributors are stockpiling. Many manufacturers, facing longer lead-times, would stockpile if they could. Shifting and surging demand has exceeded production capacity in several product categories. Many owners of capacity perceive these shifts are temporary. Current capacity is being maximized, but not much is being invested in new and more. The output of that maximized capacity is sometimes not being loaded because supplies of packaging materials are short (more).

Whatever is ready for delivery is often delayed. From fuel to furniture, shipping capacity — sometimes flow capacity — has been constrained by lack of conveyance (truck or ship or plane) or lack of containers or insufficient space for the number of containers ready to ship. This turmoil has also significantly increased the price of shipping each container that is shipped.

My best guess is that this disequilibrium will broadly persist until Christmas. If, when, and where covid is contained, demand and supply will gradually rebalance as a pandemic-fueled fixation on “stuff” is relieved by more opportunity to consume experiences (e.g. travel, restaurant dining, live music, and such). I can even imagine excess inventories prompting some deep post-holiday discounting.