This is the fifth post in a series examining the supply chain resilience reports released by the White House on Thursday, February 24.

The Department of Energy sectoral supply chain report gives less attention to current energy vulnerabilities than to transitioning from fossil fuels to clean energy. Achieving clean energy objectives is seen as enhancing national resilience to climate change, reducing US dependence on the global fossil fuels market, and more sustainably assuring energy resources for long-term US demand. As the report states:

Global energy end-use continues to be highly dependent on fossil fuels. In the United States, as of 2020, about 79 percent of primary energy end-use and 60 percent of electricity generation came from fossil fuels, including petroleum, natural gas, and coal (EIA, 2021). Multiple countries, including the United States, have pledged to achieve net zero greenhouse gas emissions by 2050 to keep the global temperature change below 1.5 degrees Celsius and avoid catastrophic global climate change. Achieving this goal will require massive deployment of clean energy technologies and an accompanying scale-up in their supply chains, both domestically and globally (IEA, 2021).

The DOE report acknowledges this transition will take several years. Meanwhile, there is a continued need for robust and resilient flows of fossil fuels. This is a particular concern in case of a large-scale catastrophe (aka “My Problem“). For example, how do we fuel water pumps, electric back-up (including telecoms), and trucking following an 8.0 plus seismic event involving a large population?

There are plenty of other risks for which current fossil energy capacity is crucial. Yesterday, March 9, US Secretary of Energy, Jennifer Granholm, told a Houston energy conference:

We are on a war footing—an emergency—and we have to responsibly increase short-term supply where we can right now to stabilize the market and to minimize harm to American families. That means releases from strategic reserves across the world, like we’ve done. And that means you producing more right now, where and if you can… we’re serious about decarbonizing while providing reliable energy that doesn’t depend on foreign adversaries. That means we’ll walk and chew gum at the same time. So yes, right now, we need oil and gas production to rise to meet current demand (more and more and more).

Three relevant factoids:

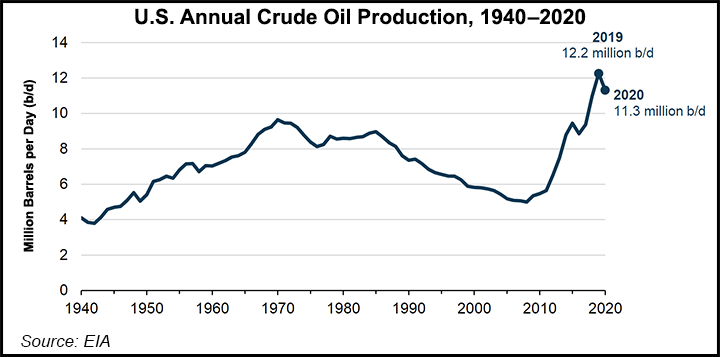

Current US fossil energy production capacity is strong. Before the pandemic dampened demand, US crude oil production was at a historic high and continues to be close to half-century highs.

Prior to the pandemic, US refining throughputs were strong. This capacity continues to be available.

National distribution capacity for fossil energy is constrained but sufficient for ordinary demand. Today there are — very roughly — 100,000 tank trunks operating in the United States. This compares to about 85,000 in 1980. Pre-pandemic the volume of gasoline being consumed was about one-third higher than in 1980. US pipeline miles for refined product have essentially not changed in this century (pipeline miles for moving crude oil have expanded). We are doing more with the same or proportionally somewhat less. In a pinch, our margin for error is also less.

The policy of the US government — and many private investors — is to accelerate clean energy capacity. There are good reasons to do so. It is also reasonable to recognize that this will be a treacherous transition, with or without WWIII. Supply Chain Resilience principles emphasize diversity, adaptability, and agile, creative self-organization.