In February 2020 we could have preserved flow. Pre-pandemic global demand had been strong. Processing, manufacturing, and transportation slightly lagged demand, but just enough to keep everyone busy.

By late February last year, flows inside China were recovering from a drastic, but brief hiatus. If North American, East Asian, and European demand had kept pulling, the push of supplies — both global and local — would have soon resumed typical seasonal patterns. First quarter global flows are usually comparatively slow.

But demand suddenly and deeply contracted. Existing orders were canceled. Deliveries were left unclaimed. Empty containers were not returned. Orders for future deliveries were not sent. Planes were parked. Ocean crossings were canceled. Assembly lines were slowed or stopped.

In an earnest effort to minimize circulation of a deadly virus, circulation of people was discouraged. This caused a sudden shift in circulation of money too. Well-established pull channels dried up. Other channels flooded. What was being pulled from where and how it was being pushed, changed in an economic blink-of-the-eye.

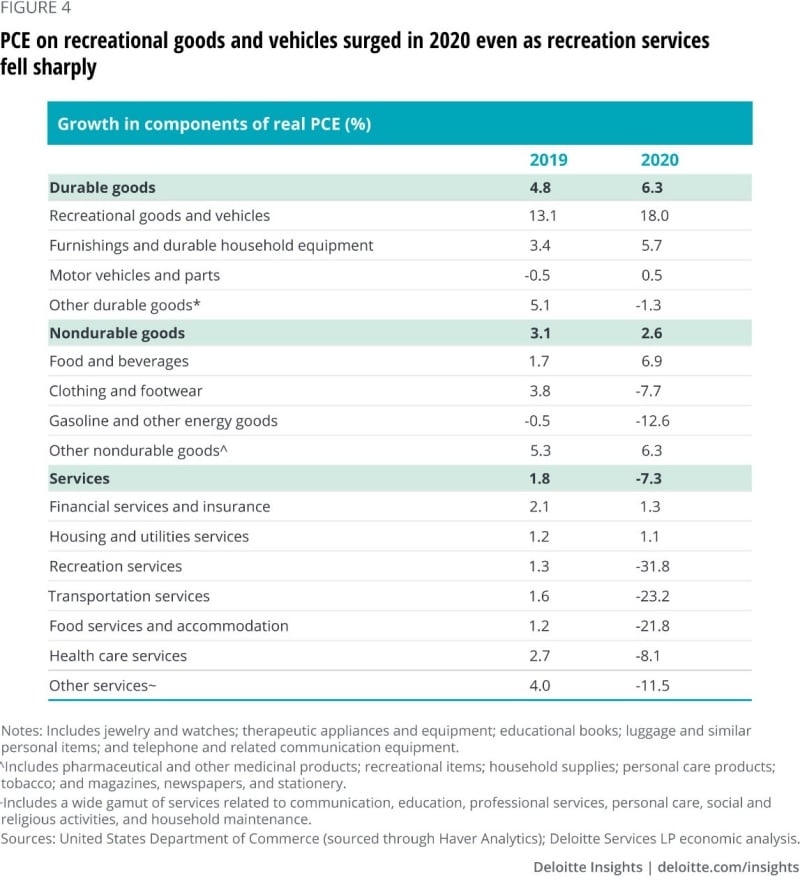

Unemployment soared, especially among the most consumer-facing service sectors. To preserve lives and livelihoods, more money was pushed out. Given radically altered options for expressing demand, this mostly resulted in an increased savings rate and increased consumption of a few narrow categories of durable goods. Many of my neighbors now have new guns, recreational vehicles, home improvements, and electronic gadgets. They are not alone. See Deloitte’s analysis of Personal Consumption Expenditures immediately below.

Responding to these unpredicted — unpredictable — sharp shifts in demand has been complicated. A persistent shortage of upstream containers has constrained flow recovery. Disease and self-quarantines among stevedores and drayage drivers has slowed movement through many ports. Container ships are waiting longer to embark and disembark. Retiring truck drivers and closed driving schools have reduced capacity available for almost every component of flow. In many cases, demand has been volatile, suddenly surging in one category and as suddenly shifting to another category. Each incremental pinch narrows overall push. Sudden pulls for one product tend to skew adjacent flows too.

So, it is not surprising that the inventory to sales ratio remains so depressed. Joseph Lupton at JPMorgan recently wrote, “While non-manufacturing activity is now tracking a strong and steady recovery, the goods-producing sector has been buffeted by supply constraints alongside continued boomy gains in final demand… The result has been a slump in inventories that, over the past two decades at least, looks to be unprecedented outside of a recession.”

Reflecting that “boomy” unevenness of demand, it also makes sense that there is accumulating evidence of selective stockpiling. How much of this might be Stermanesque (Doganic?) “phantom ordering”? And if so, how badly and widely might this unwind? In late July, John Dizard worried aloud in the Financial Times, “The inventory en route around the world defies the imagination, not to mention the antique information systems in the shipping business. All of that fitfully tracked and delayed stuff, when it finally lands where it is supposed to, looks as though it will create a big enough pile to trigger a bad inventory recession, where demand for goods drops while accumulated stockpiles are run down.”

Short of Dizard’s worst case, the current disequilibrium of supply and demand is likely to generate chop in many channels well into March 2022. And even this projection depends on Delta’s surge peaking as previously experienced in the UK and India. If Delta persists or post-Delta is worse, stand by for storm surge and drought and absence of anything that looks or feels like flow.

A fragment attributed to the ancient Greek philosopher Heraclitus reads πάντα ῥεῖ (panta rhei) or “everything flows”. Some suggest a better translation is “everything is flux.” Most of us find ourselves very much in flux. Some of us are happy with this, Dizard quotes one supply chain player as saying, “For me, the more chaos, the better.” But many others would prefer to recover flow.

In explaining Heraclitus, Plato points to Rhea, mother of the gods, as the source of what we now hear as flow or flux. In the classic myths Rhea overcomes murderous disorder, personified in her husband/brother Kronos (god of time and more), through a shrewd distraction. Flow transcends Time’s fearful greed by seeming to sacrifice what she carefully saves. Just-in-Time? Just-in-Case? Or flexible enough to strategically benefit from disorder. (More)

Early in the pandemic a local retailer simultaneously advertised a sale price for its private-label toilet paper while restricting purchases of all TP brands to no more than two twelve packs (or the equivalent). This fully satisfied the needs of most consumers and seriously reduced the “fearful greed” of a few. The combination of no more empty shelves plus the supply confidence implied by the sale price transformed recurring deficits into persistent flows.

Whoever deployed that paradoxical demand management tactic is a latter-day Rhea.