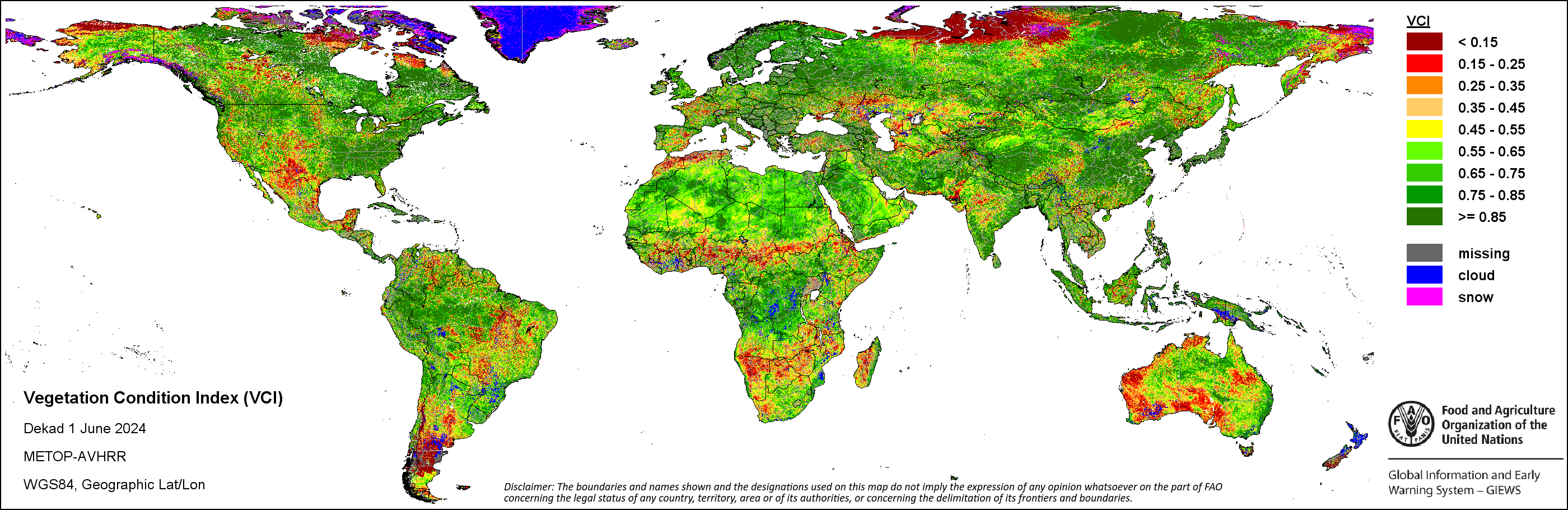

According to the USDA, during 2024 the world is leaning toward a bit less wheat, corn, and soybeans. But existing stocks will mostly fill the gap. There will likely be a bit more rice. But whether up or down the shifts are under one percent on huge volumes. Large-scale, short-term weather and crop conditions look okay in most high-production places (see map below). According to the World Meteorological Organization, a transition from an El Niño to a La Niña weather pattern is underway. In the next several weeks WMO forecasts a “large-scale cooling of the ocean surface temperatures in the central and eastern equatorial Pacific Ocean, coupled with changes in the tropical atmospheric circulation, namely winds, pressure and rainfall. The effects of each La Niña event vary depending on the intensity, duration, time of year when it develops, and the interaction with other modes of climate variability. “

Last week the US Energy Information Administration wrote, “We forecast U.S. crude oil production will grow by 2% in 2024 and average 13.2 million barrels per day (b/d) for the year and a further 4% in 2025. If our forecast is realized, U.S. crude oil production would set new annual records in both 2024 and 2025.” Global oil futures — bouncing around the low to mid 80s — imply widespread expectations for sufficient supply (see Brent Crude chart below). A provocative new long-range forecast by the International Energy Agency offers:

Based on today’s policies and market trends, strong demand from fast-growing economies in Asia, as well as from the aviation and petrochemicals sectors, is set to drive oil use higher in the coming years, the report finds. But those gains will increasingly be offset by factors such as rising electric car sales, fuel efficiency improvements in conventional vehicles, declining use of oil for electricity generation in the Middle East, and structural economic shifts. As a result, the report forecasts that global oil demand, which including biofuels averaged just over 102 million barrels per day in 2023, will level off near 106 million barrels per day towards the end of this decade. In parallel, a surge in global oil production capacity, led by the United States and other producers in the Americas, is expected to outstrip demand growth between now and 2030. Total supply capacity is forecast to rise to nearly 114 million barrels a day by 2030 – a staggering 8 million barrels per day above projected global demand... (More and more.)

The IEA forecast depends on global grid capacity expanding as quickly as needed between now and 2030. This is possible, but will not happen without serious challenges — and occasional failures — along the way. There are both near-term and long-term gaps to fill, especially where demand is growing fast. ERCOT, the Texas grid operator, is an especially colorful canary in this coal mine. Spectrum news recently reported, “ERCOT says there is a 12% chance of rolling blackouts this August. Officials are also warning that demand will increase exponentially over the next several years… A 40-gigawatt increase from one year to the next in the five-year horizon. That’s effectively almost doubling the peak demand of the ERCOT grid in about six years.” (More and more and more. )

Fuel costs associated with crude at under $90 per barrel tend to result in less freight cost volatility (and related structural stresses). The gradual normalization of Panama Canal transits incrementally smooths global flows. Suez canal transits are, of course, still suppressed and down nearly two-thirds from last year. Still, despite various frictions (here and here and here), overall global trade volumes are up over slow 2023 flows (here and here). Given otherwise strong economic data, there is no particular reason to expect the real-value of US goods imports to fall far in the still underway second-quarter. The Global Supply Chain Pressure Index continues to show lower than average measures. The Cass Shipment Index has been softening but remains in its mid-range. DAT Trendlines are mixed, but big early summer increases in year-over-year load-to-truck rates are meaningful.

Millions of people are largely excluded from these robust flows. This is not, however, caused by upstream capacity constraints. Places on the periphery of big midstream channels are more likely to have problems. But absence or paucity of effectual downstream pull is the most common culprit. There are significant geo-political, climate-related, and other natural risks that could catastrophically subvert upstream capacity and midstream velocity with dangerous downstream results. But as the second half of June leans into the second half of 2024, global flows are strong.

+++

June 24 Update: Using the same or similar information sources, Peter Goodman at the New York Times offers a very different interpretation than above — or that offered in my May 27 overview — regarding freight flows. We both perceive increased friction, related congestion, higher prices, and plenty of prospects for additional risks. I tend to see high capacity complex networks morphing with volatile context. Mr. Goodman seems to see a highly concentrated, engineered system being manipulated in unsustainable ways. There is certainly some of each (and much more) going on. What is predominant? What is the straw that might break the camel’s back? What flutter of butterfly wings will facilitate persistent flows?

June 25 Update: I wonder if some Bloomberg editor explicitly decided to challenge Peter Goodman’s argument. In any case, this morning there is an alternative interpretation of supply chain stress available here. The Bloomberg piece channels Jason Miller explaining that upstream capacity is well-calibrated with (even a bit excessive considering) current demand… and midstream channels have the ability to maintain necessary flow velocity. This is suspiciously close to my own perception, so I may be hearing what I want to hear. Worth reading both points-of-view.