Unprecedented 2021 demand prompted unprecedented 2021 US flows… and plenty of related supply chain stress. During the first half of 2022 US demand has stabilized (at close to pre-pandemic trends). Flows are off their peaks and dispersed over more channels. Supply Chain stress is reduced. The United States is, however, still pulling much more push than pre-pandemic.

The west coast Longshore and Warehouse Union contract expired July 1 (more). Work continues while negotiations continue. Just in case (and looking for dock-space and available rail freight) some shipments have shifted to US Atlantic and Gulf coasts. Overall inbound US flows are within 5 to 10 percent of 2021 all-time records.

There has been — still is, in some quarters — concern that China-US flows are constrained by counter-covid measures in China. But overall US imports from China have remained well-above pre-pandemic levels, even as maritime rates (more) have fallen from stratospheric to merely well above “ordinary” (whenever that was).

It is increasingly clear that reduced US demand for many China-sourced goods has coincided with the friction caused by China’s lock-downs (more and more and more). There is still an opportunity for upstream capacity constraints to complicate downstream fulfillment this Christmas, but those yin/yang proportions are unlikely to be clear for another eight to ten weeks.

Meanwhile a strong dollar makes imports cheaper. The US is spending more on imported food than ever before, about one-third more than pre-pandemic. But the US is still more than 80 percent self-sufficient on most foods — and remains the planet’s largest exporter of food-related products.

Domestic and global food flows are troubled by weather related constraints in many places and war-related disruption of Ukraine’s huge grain exports. It is, however, too early to be confident — either way — regarding Northern Hemisphere 2022 harvest conditions. Yesterday’s USDA Crop Progress Report is mixed. AgWeek headlined, “spring wheat improving, slight decline in corn, soybean conditions.” Wheat futures have fallen considerably from their February 28 high — and consistently since early May — but current prices remain much higher than decade-long averages (more). Yet even with recent softening, global food prices have increased farther and faster than US food prices.

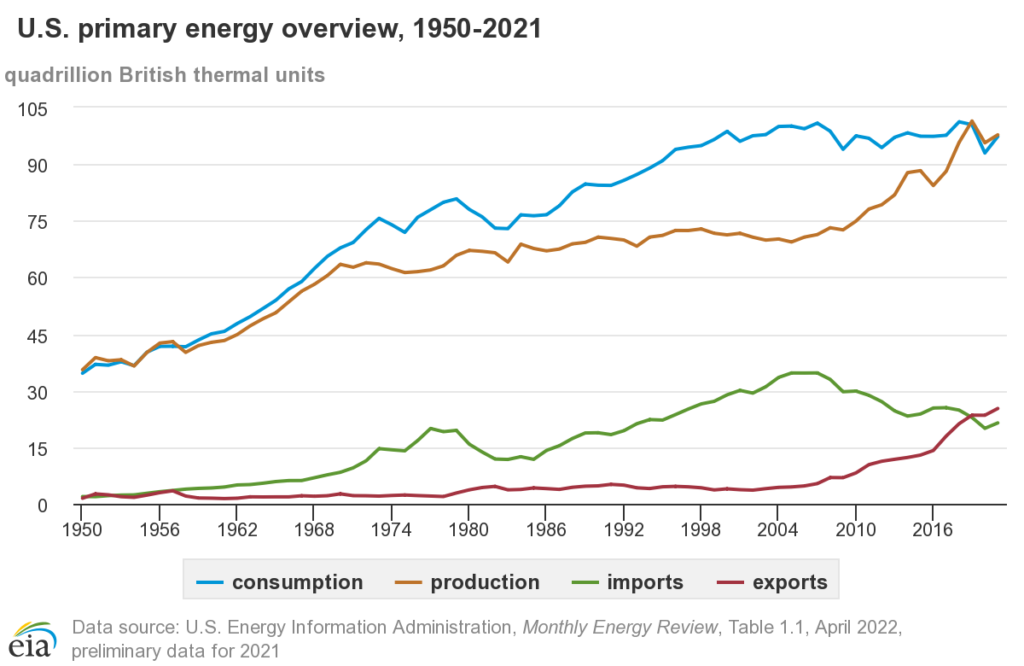

The United States is also mostly self-sufficient in energy. Since 2019, for the first time since the 1950s, the US has produced more energy than it consumes. (See the chart below.) The nation still imports about one-fifth of domestic energy consumption, which helps balance demand and supply by securing beneficially priced crude or finished products for specific seasons and regions. In 2021 79 percent of total US energy consumption was supplied by fossil fuels. US refinery capacity is currently very tight and operating at unusually high utilization rates (more and more and more).

Global energy flows are beginning to adjust to disruptions and diversions related to the war in Ukraine and the weaponization of energy supply chains. Discounted Russian fossil fuels are finding customers. European demand is — so far — being fed by new non-Russian and diminished legacy flows (more). Yesterday the WTI benchmark price for oil fell under $100 for the first time since April. (Even as natural gas prices continue to soar.)

In terms of domestic transportation of food, fuel, and more, pipeline capacity has improved. Rail capacity is diminished by congestion (more). The United States currently has more trucks and truckers operating than ever before, but spot market flexibility is starting to be shed under pressure of diesel prices and reduced demand.

It is, of course, much more complicated than this audacious summary. Risks abound. Fresh opportunities beckon. Some consumers are falling off the edge as this is being written, while others are indulging. But right now (early July), right here (continental United States), demand is more doable because there is a bit less of it and because we expanded push capacity trying to fulfill last year’s pull.