Deutsche Welle tells us: “Water levels in the Rhine River are just inches away from forcing another shutdown of ship transportation.” Freight volume at Rotterdam was basically flat in the first half of 2022. Loss of the riverine connection, especially if early in the second half, would further narrow flows.

Slower and lower flows characterize many aspects of a Europe once again at war and worried about what’s ahead.

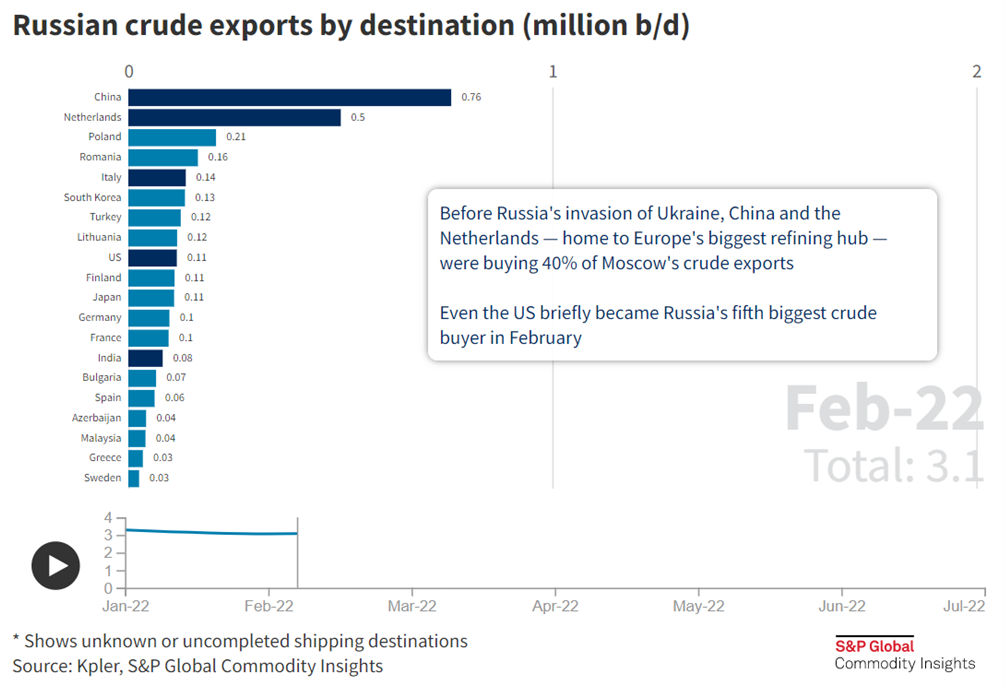

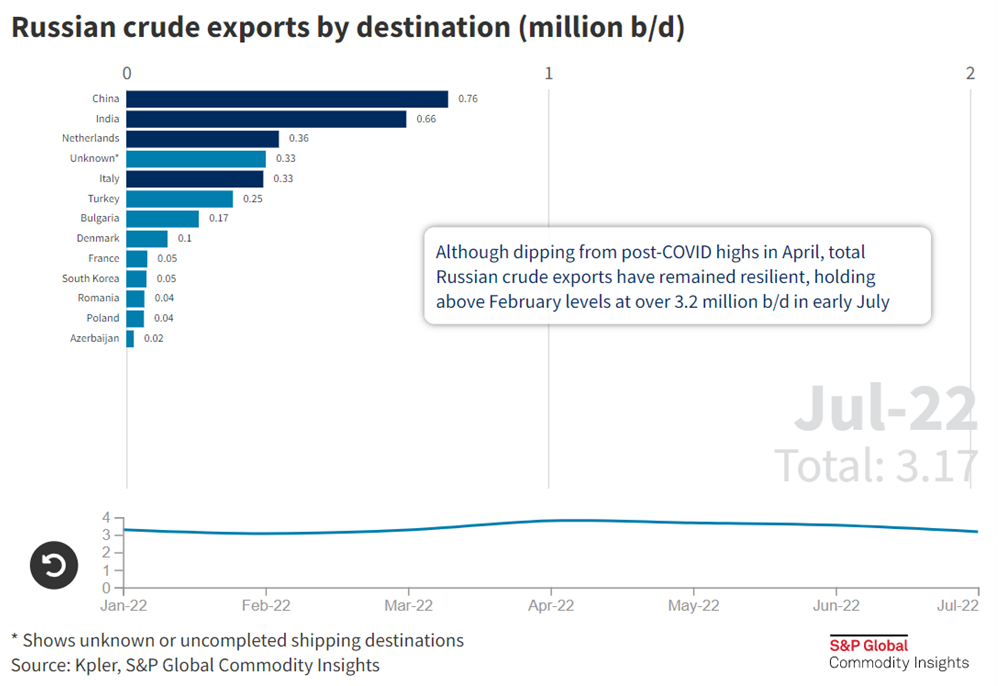

As this blog has repeatedly reported, Russia’s oil — despite various sanctions — continues to flow. More effort is required to buy it, but it is still sloshing about the world. Below are charts from S&P. (The original S&P resource is interactive and very much worth accessing, please also see the shifting sources of European oil imports since February.)

Yesterday there was good news that Nord Stream 1 has resumed operations (more and more). For now the flow is one-third or, perhaps, two-fifths of heretofore, but Europe is happy to get it here and now. Tomorrow is another day.

More good news — or at least progress toward potential good news — in releasing more flows of Ukraine’s grain to world markets, especially customers in the Middle East and Africa. Today a Turkey-brokered agreement will be signed in Istanbul. According to France24, “A coordination and monitoring centre will be established in Istanbul, to be staffed by UN, Turkish, Russian and Ukrainian officials, which would run and coordinate the grain exports, officials have said. Ships would be inspected to ensure that they are carrying grains and fertiliser rather than weapons. It also makes provision for the safe passage of the ships. The control centre will be responsible for establishing ship rotation schedules in the Black Sea. Around three to four weeks are still needed to finalise details to make it operational, according to the experts involved in the negotiations.”

Disrupted channels are the most common complication facing high volume (and especially high velocity) demand and supply networks. Severe reductions in discharge of Ukraine’s grain are a dramatic example. But what we also see is that where effectual demand and production persists, the flow of supply may twist, turn, and cuss, but continue…

BELOW: FIRST FEBRUARY, SECOND JULY