[Updates Below] Europe’s need to replace lost Russian energy supply has discombobulated markets, channels, and global flows. Nervous demand wants to pull more energy than long neglected and currently disrupted fossil fuel capacity can confidently — affordably — fulfill (more and more and more and more and more).

As a result of Europe’s precipitous pull on non-traditional channels (skewed by the prospect of a war-time winter) fuel prices are higher — which limits the ability of demand to pull much harder. European uncertainty regarding the ability to pull sufficient flows to fulfill minimum social and economic needs is a principal cause of global energy price volatility.

Given China’s zero-covid policies (more, and strengthened statism), Europe’s recession, and an induced counter-inflationary US economic slowdown, net global demand for energy is likely to remain off-peak for months ahead. But local shortages and price surges are also likely as mostly fixed capacity tries to adapt to (and exploit) the turmoil resulting from Russia’s invasion of Ukraine — and all its cascading consequences.

With care the behavior of this complex adaptive system can be broadly anticipated. It cannot — will not — be precisely predicted. In a personal effort to perceive emerging strategic context, I will give recurring attention to:

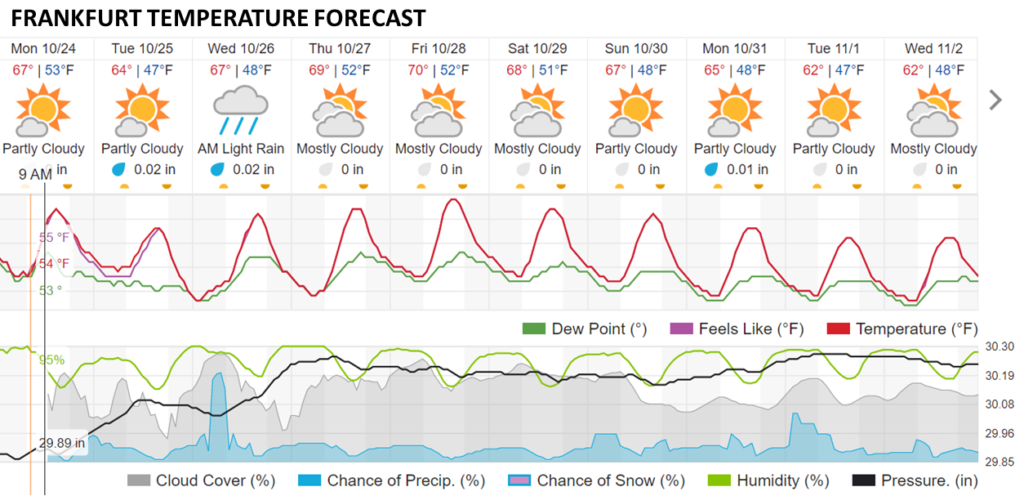

Frankfurt, Germany’s temperature (more and more, see below). This may be a meaningful indicator of energy demand in Europe’s densely populated industrial heartland.

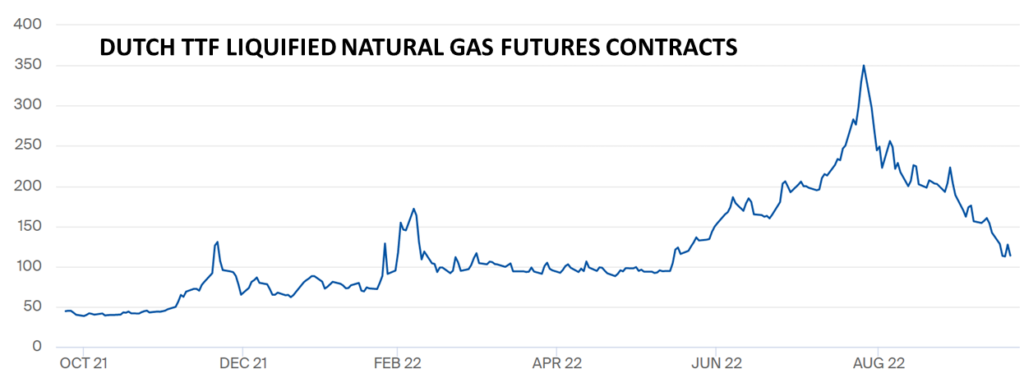

Liquified Natural Gas (LNG) price futures, especially at Rotterdam (Dutch TTF, see below) and in comparison to the US Henry Hub. LNG constitutes a significant replacement proportion for lost Russian natural gas flows. Higher prices will signal supply falling below demand and/or fear of insufficient supply (more and more).

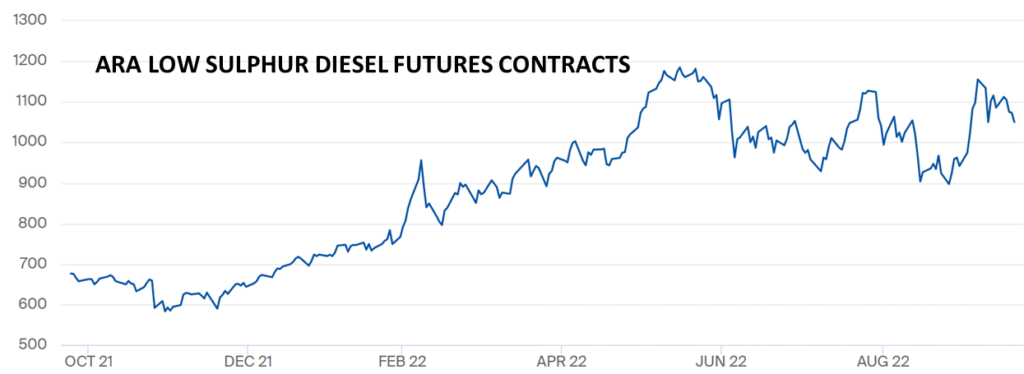

Diesel price futures, especially comparing Amsterdam-Rotterdam-Antwerp (ARA, see below) to New York Harbor ULSD. Even if LNG flows mostly match lost natural gas flows, there are myriad potential energy gaps. Diesel is a flexible gap-filler. But low diesel inventories and limited production capacity may be unable to close some crucial gaps (more and more).

Taken together these sources may provide early warning signals in terms of shifting directional balances between global demand and supply (admittedly with a trans-Atlantic bias).

+++

October 25 Update: Nice summary of immediate petroleum market realities from Bloomberg. Below is an Infographic from S&P Global that clearly complements the situational assessment I offered on Monday morning.

October 26 Update: Very helpful summary by S&P Global of the significant shifts in global demand for LNG as a result of Europe’s need to replace Russia’s pre-war supply of natural gas.

November 4 Update: Warm temperatures, less-heated economic behavior, full storage tanks, and better-than-expected supply have continued to suppress Europe’s immediate thirst for LNG. More than thirty LNG vessels are cycling off Europe waiting for prices to increase — some are even giving up and heading toward Suez searching for better markets farther east. EU access to LNG-alternatives — such as here and here — are watched almost as closely as the weather.