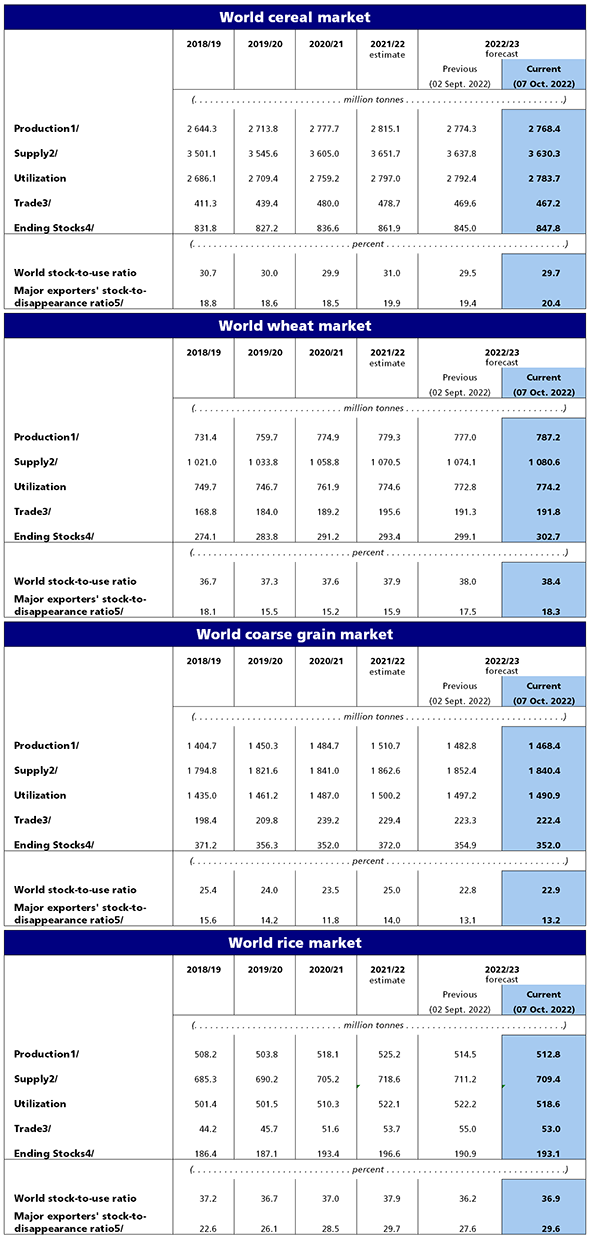

Demand is strong. Supplies are disrupted, but — so far — sufficient. Prices are comparatively high, but not as high as earlier this year. The September Food and Agriculture Organization’s cereal production forecast is close to the high end of the last decade’s volumes, but slightly less than last year (see charts below, more and more).

Several key channels for shipping food are constrained. Black Sea flows are limited by war, but since July an agreement brokered by the United Nations and Turkey has facilitated 285 shipments from Ukrainian ports carrying 6,429,098 metric tons of grains and other foodstuffs. (The current agreement will sundown in November unless renewed.) Canada’s rail capacity is struggling to deliver the flow needed for a strong harvest. Significant drought in both the Danube and Rhine River basins has reduced yields, complicated barge transport, and reduced supply velocity. The Yangtze River is also running very low (more). In recent weeks there have been more low-water closings than usual on the Mississippi River. Urgent dredging has been required to reopen flows. (To be sure, extreme weather is an equal-opportunity threat: floods have complicated commodity flows in Australia, Pakistan, and Thailand).

Food demand is often constrained by the consequences of a very strong US dollar. In more affluent nations, such as the United Kingdom and Japan, the cost of food imports, often priced in dollars, has increased substantially over the last six months. In less affluent nations, such as Lebanon and Sri Lanka — with sparse dollar reserves — the ability to pay is being tightly squeezed or exhausted (more and more).

In 2022 enough food is being produced to feed the world’s population. But production patterns are becoming less predictable as climate change accelerates and production costs increase (more). Sufficient distribution capacity exists, but is vulnerable to a wide variety of potential disruptions. Distribution capacity is especially shallow and fragile where the ability to express effectual demand — in other words, the ability to pay market prices — is weakest. According to some credible sources, of almost 8 billion residents of the planet, about four out-of-ten cannot currently afford to purchase a healthy diet.