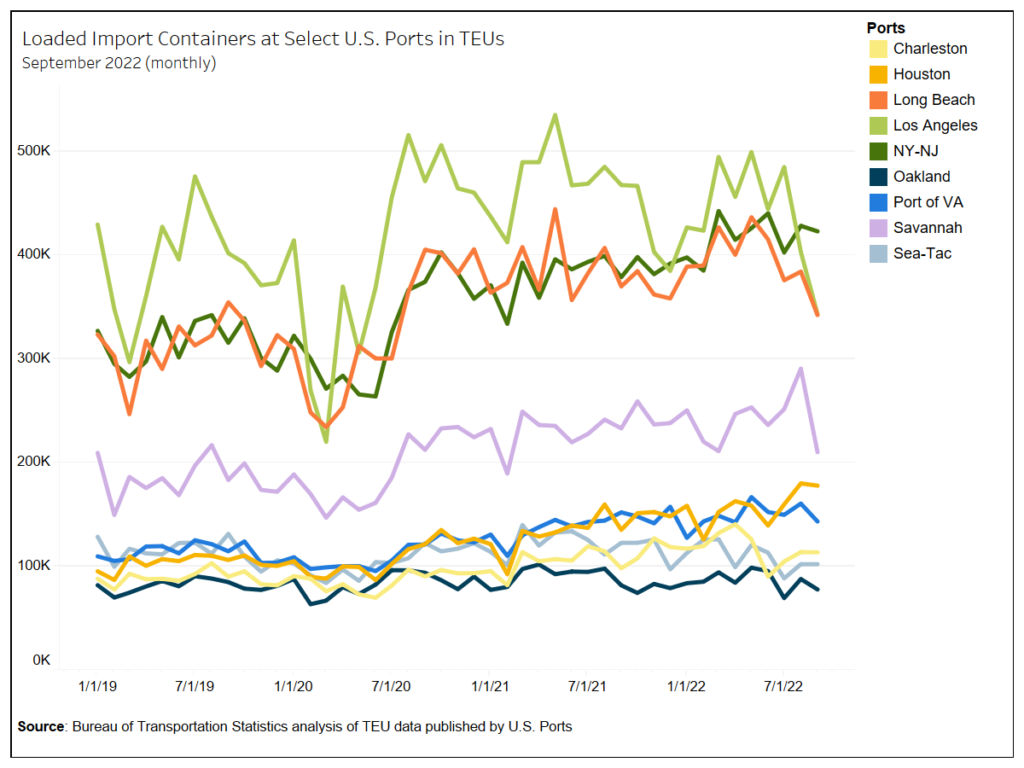

[Update Below] Over the last year, inbound maritime flows to the United States have slowed and dispersed (see chart below). This adaptation seems to be accelerating in the current quarter.

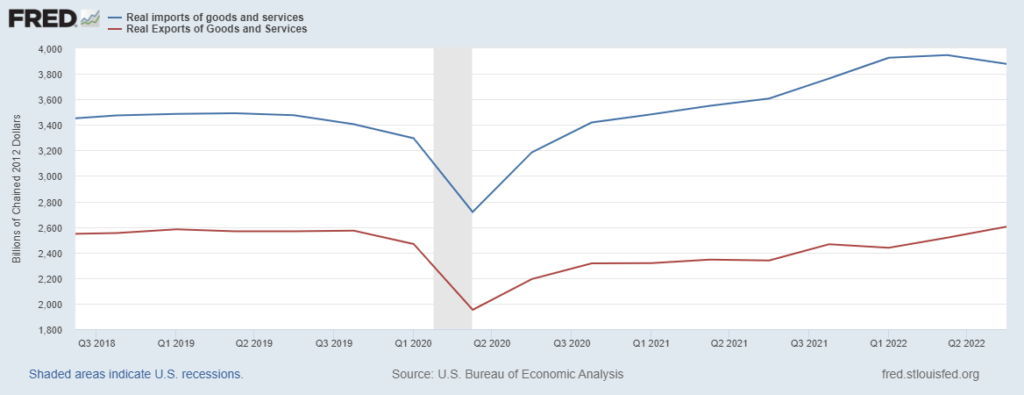

Recently declining demand for imports is behind the slowdown (see second chart below). The dispersion is part of a long-term trend. Demand-pull is usually fickle. Supply-push is inclined to be stubborn.

According to S&P Global, even as West Coast ports have experienced declining volumes, “South Carolina Ports handled 256,879 TEU during October… up 9% against the year. Loaded imports came to 121,305 TEU, up just under 13% on the year. October was the third busiest month in the port’s history. Elsewhere, the Port of New York/New Jersey moved 842,219 containers in September, over 130,000 more than the Port of Los Angeles during the same month.” (More and more.)

Dispersion arguably began in 2016 when new and larger locks allowed for passage of much bigger container ships to and from Asia through the Panama Canal. Pandemic pressures have accelerated use of alternatives to the Ports of Los Angeles and Long Beach (pre-pandemic it was typical for more than 40 percent of US container imports to be received at LA/LB). Intense congestion at LA/LB encouraged diversion of flow to ports other than San Pedro Bay. The ongoing threat of labor action at all US West Coast ports has reinforced this choice. A possible US rail strike would quickly cause congestion at just about every US container port, but West Coast inbound is especially dependent on long-distance rail to distribute East Bound flows.

So… while it took awhile to find, schedule, and coordinate vessels, drayage, warehousing, and surface transportation, over the last year-plus many US importers have spread their risk. Now that congestion is gone, LA/LB can reassert its innate proximity advantage for East Asian sources. Once the risk of labor action is resolved, US West Coast ports will reclaim some proportion of total flows. But the newly expanded US Gulf and East Coast channels will not be abandoned. They also have an innate comparative advantage in their proximity to many million US consumers.

[Soon to come: US Outbound Flows… especially via the Mississippi River]

+++

November 22 Update: Bloomberg reports: “Ports on the US West Coast could permanently lose as much as 10% of the seaborne cargo that has been diverted to the Atlantic coast amid logistics bottlenecks, regulatory headwinds and labor uncertainty.”