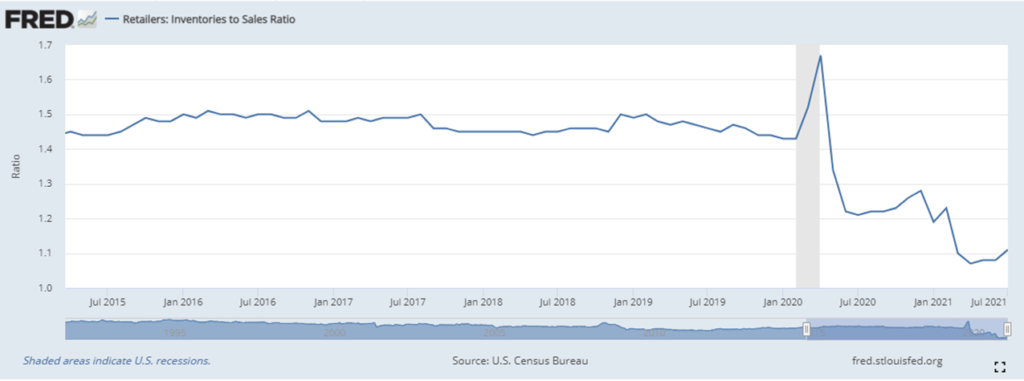

Here’s the final paragraph in a September 27 WSJ report: “Year to date, new orders for durable goods are up 24.7% compared with the same period a year earlier. Shipments, meanwhile, are up just 14.1%.” Buried lede? It is for me.

Here’s the source report from the Census Bureau. Demand is up one-quarter. Supply is up about one-seventh.

Despite all the raw material, production, packaging, shipping, workforce, and other complications, total durable goods shipments are up more than 14 percent year-over-year. Remove the transportation category and orders are up a bit less than 18 percent and shipments are still up about 14 percent

The semiconductor shortage has seriously undermined the ability of automobile manufacturers to flex capacity to meet demand. But in most other categories — even with all the friction widely noted — shipments are within spitting difference of orders. In some cases demand and supply can be seen kissing: During August the computer and other electric products category shipped goods worth $208 billion against new orders worth $177 billion. Product offerings and inventories are being rebuilt.

Enough for this holiday-season? Perhaps not. But existing capacity is being well-deployed.

Will the recent demand surge for durable goods endure? I don’t think so. Exploiting current bottlenecks to maximize existing capacity makes enormous sense. Investing in huge, quick, expensive capacity expansion makes much less sense… for many, even most, categories.

Oxford Economics has released a very helpful supply chain stress indicator. According to their September 22 report:

With our tracker showing stress still rising, supply-chain headwinds look unlikely to ease in the near term. But we see a light at the end of the tunnel – current challenges will not be indefinite. As vaccination rates rise in the US and overseas and demand slowly returns to pre-pandemic patterns, transportation logjams will clear, input costs will normalize, and production and hiring challenges will recede. In other words, easing supply-side constraints, rising capital investment, and demand normalizing to pre-pandemic patterns will allow firms to clear the significant backlog of orders that have built up in the past 18 months.

How long this will take depends on the category — and the character of demand waiting at the end of that tunnel.