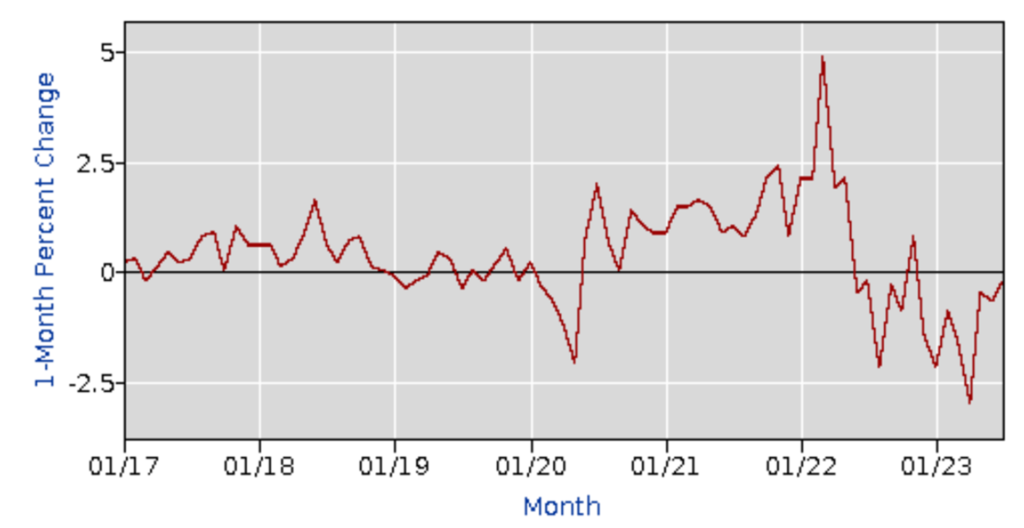

Inflation-adjusted July Personal Consumption Expenditures on Food-At-Home once again increased slightly (see chart below). If we continue to see these “slight” increases for a couple more consecutive months I will have to retire my use of “flat” to characterize the current slope. But this July our real PCE for food was $1032.4 billion while last July our real PCE was $1027.9 billion. That’s still flat enough for me. What’s less than $5 billion among friends and fellow citizens?

Here’s how Bloomberg explained the PCE results:

Low unemployment, pandemic-era savings and wage growth are providing Americans the wherewithal to keep spending, allowing the economy to power ahead. Many economists have had to push out their recession calls, or in some cases, scrap them altogether as a result. The latest figures point to a strong start to economic growth in the third quarter… The saving rate decreased to 3.5%, the lowest since November, suggesting the recent pace of spending may not be sustained in coming months. Pandemic-era savings are dwindling, the labor market is cooling, delinquency rates are rising and the resumption of student loan payments this fall threatens to further strain consumers’ finances. Retail executives have suggested as much and remain cautious about the outlook.

If Bloomberg is right I should be able to keep using flat or falling into the Autumn.