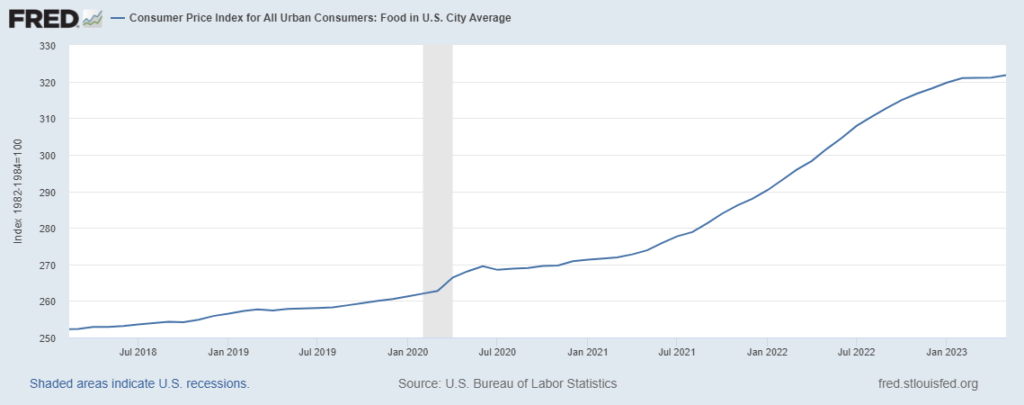

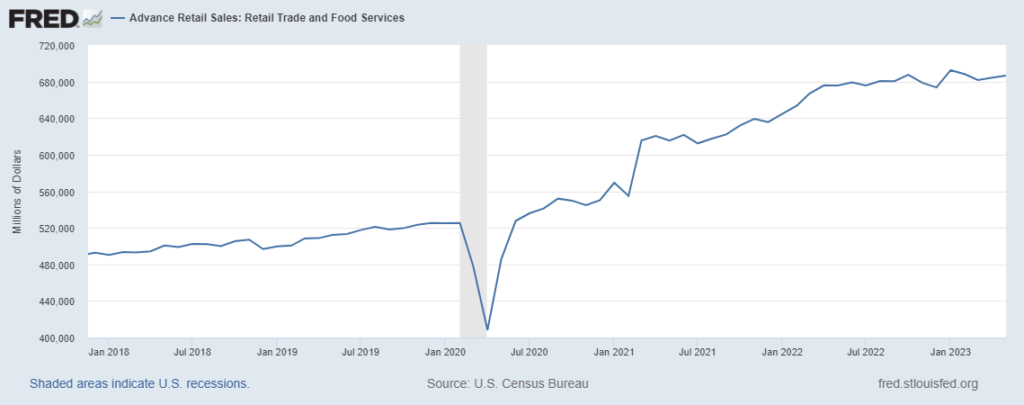

Americans continue to eat more — or at least spend more on — Food-At-Home. But our rate of increase has slowed considerably (see chart below). In May 2019 US consumers spent $981.7 billion (2012 dollars) on groceries and related. Last month we spent $1023.5 billion in 2012 equivalents. This is a bit more than a four percent increase (as we avert our eyes from the turmoil between then and now). From May 2015 to May 2019 real spending on food increased just about ten percent. Due to inflation it can seem like we are spending even more on food (again, see chart below). But for most of the last year our real, inflation-adjusted expenditures for food have been flat or falling… and as a result, food supply chain dynamics have been much more predictable. Current production and distribution capacity has been well-matched with demand.

{kind=link}

{kind=link}